Twenty years ago, the SPL was on the verge of meltdown. A lucrative spell of TV revenue had created a culture of excess, of arrogance, and the belief that the league’s value had grown, perhaps beyond the size of the market in which it resided.

In 1998, Sky had bestowed upon us a £48m, four-year deal. With that cash, clubs pushed the boundaries of what they could borrow. And with that, wages-to-revenue ratios edged ever further into unsustainable levels.

And yet the league was arguably never better in terms of top-to-bottom quality. Celtic and Rangers had strong squads, attracting the type of player that just wouldn’t be possible today. They were supplemented by a robust, talented Hearts side, a youthful and developing Hibs and an ambitious Motherwell and Livingston.

The good times were seemingly here, particularly after an independent report commissioned in 2001 suggested that the SPL could double or even treble what was currently on offer when renewal time came around in 2002.

Sky thought differently. The offer presented to the clubs was a continuation of the status quo; £48m, four years. The clubs, on the strength of their report, and emboldened by their hubris and their desire to spend even more, rejected the deal, expecting a counter-offer which never arrived.

Unlike today when there are multiple options available (whatever their individual merit), Sky were the gatekeepers, and they knew it. They were already concerned about the audience size beyond when Celtic and Rangers played, and were also wary of the scenes at Celtic park in 2000, when the late-season derby effectively settled the title and the 6.05pm kick-off had led to carnage in and out of the stadium, not least referee Hugh Dallas being struck by a coin.

So when the clubs responded with such ambivalence, Sky were unmoved. The Premier League was everything to them and they understood the dynamic far better than the Scottish clubs did.

So, what now?

SPL TV

You can revisit the full story of what SPL TV was in the first issue of Nutmeg; this is more a story of what it could be now. Because, 20 years on, the discussions persist. There is consistent debate as to whether the concept could work for us now, considering nothing much has gone right since that Sky rejection.

The SPFL’s current deal, signed in 2018, is a five-year, £125m agreement split among the 12 top-flight clubs. When compared to similarly-sized European countries, our per-season rate is markedly smaller than the likes of Denmark (£45m), Sweden (£46m), Greece (£50m) or Norway (£60m). But there are also a few caveats; Scandinavian nations show practically every match live, whereas Sky shows only 48 SPFL games per season.

That is because these are national broadcasters and it allows them to fill schedules with as much football as possible. Sky don’t have that relationship with our game and only show what they can be bothered to, even if it means key midweek rounds of fixtures aren’t aired at all. The cost-benefit analysis, as far as they are concerned, isn’t worth it and it doesn’t really seem as if their indifference is likely to change any time soon.

When looking at alternatives, BT Sport are always mentioned and their coverage was indeed more loving and downright enjoyable than Sky’s offering, but the simple fact is that they had the chance to share or grasp the rights in 2018, only for their offer to be described as ‘derisory’ by those close to the bidding. So BT might have shown the SPFL some love, but they didn’t want to pay for the pleasure. The way in which their business has developed since, it’s highly unlikely they would get back involved.

The BBC provides a small sum for the highlights packages, while Premier Sports have held rights to the League and Scottish Cups for this season but it is another cost for the consumer over and above existing packages, and it feels wrong that yet more money is being spent on the product in Scotland.

As well as Sky Sports and Premier Sports, from 2024 you’ll need another subscription with the Nordic broadcaster Viaplay in order to watch Scotland’s national team matches. The burgeoning company – which is yet to even launch in the UK – has secured the rights for four years for all World Cup and European Championship qualifying, as well as Nations League fixtures. For us, the consumers? Simply another cost to take into account.

So could going it alone now be the option? Is SPL TV the answer?

I spoke to representatives from various media companies to ask their opinion on issues that would either encourage or prohibit the concept of SPL TV (or SPFL TV, to use modern parlance) from becoming a success now.

COST

The SPFL clubs currently generate in the region of £30m per season including the deal with Premier Sports for League Cup and Scottish Cup rights. That would be quite the gap to fill from the very beginning, and while Rangers and Celtic will hardly need it to survive (indeed their cut of the money would only pay a fraction of their respective wage bills), others will have come to rely upon it.

Which would mean a competitively priced but aggressive subscription campaign from the start, encouraging as many sign-ups as possible to bridge the gap. With all that being said, clubs may have to accept a period of short-term pain for long-term gain.

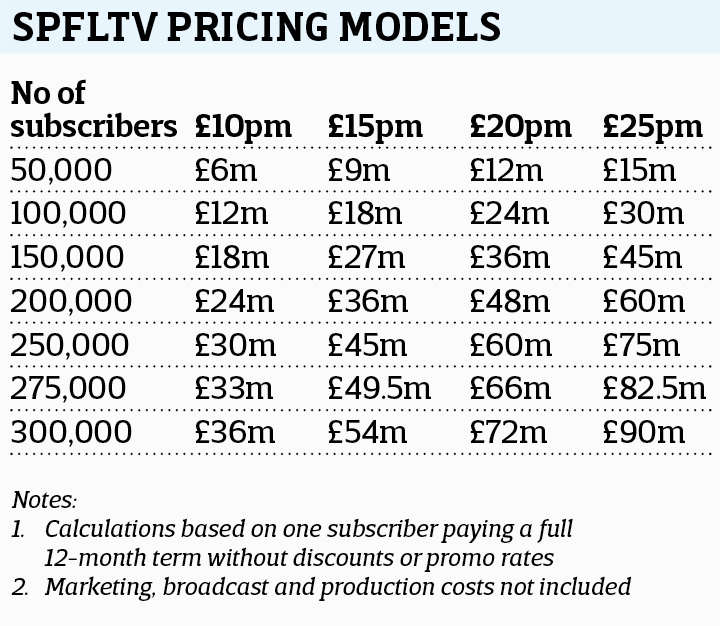

What of the pricing model? Well, the coronavirus pandemic led to clubs charging anywhere up to £15 per match to watch online when attendance in stadiums was not allowed. That may prove excessive in the long term but also suggests an appetite for pricing in excess of what a consumer may pay for Netflix, Amazon or other streaming products.

If SPFL TV offered every match, plus a host of additional options, then a pricing model of £20 or perhaps higher could be sustainable.

There are of course heavy caveats to the pricing model below. There would have to be an aggressive marketing drive from the league itself to acquire those subscribers, rather than leaving it to the carriage channel to do all of the heavy lifting. This would carry a significant cost beyond what is currently being spent.

There would also likely be introductory rates and offers of discounts to customers who may want to leave or cancel during the summer when there is no football. Finally, the league would need to inherit the costs of broadcast and production, as well as the initial setup of their own direct-to-consumer digital platform. These are costs which cannot be ignored.

Even still, at the higher end of subscription costs and subscribers, you can see how the idea of SPFL TV would be alluring to everyone concerned.

SELF-PROMOTION

The other inherent advantage that SPFL TV holds over deals with a rights holder is the ability to self-promote. Sky’s appetite for doing so beyond the Old Firm has always been tenuous at best, particularly when only broadcasting 48 games across an entire season.

With the power to drive innovative marketing techniques and encapsulate all the elements that make Scottish football great, there is inherent power in creating the correct image for the game, one which is regularly discussed and recognised online but is rarely, if ever, reflected in the actual advancement of the game itself.

PRODUCT

Imagine a channel where nobody is required to prove themselves to anyone, a channel where the subscribers are already fans of the product and the atmosphere is celebratory of Scottish football, rather than clamouring for relevance amidst the English Premier League noise.

It might be smaller in the outset, and require audience building, but the ability to tell the stories no broadcaster has time for is powerful. Coupled with a smart non-matchday offering, akin to the irreverence but undeniable love shown by the likes of A View from the Terrace, and the sport may find an audience beyond its base given its penchant for the, at times, unconventional. F1’s Drive to Survive demonstrates the fact that fans can be found if the content is engaging.

But there is literally zero experience of doing this within the current leadership. A talented, innovative content creation team would need to be put together to accentuate the positives and provide unequivocal value for money for the consumer, even at a lower price point.

SUBSCRIBERS

Those I spoke to were at pains to state that the size of the ‘overseas’ Scottish football audience – that is, expats – is largely overblown and an overreliance on a significant level of sign-ups from the US, Canada or Australia would be dangerous.

But even at the top end of the model, the magic subscriber number of 300,000 doesn’t seem completely unachievable if the product is good and consumers can justify the spend. At the moment a Sky subscription incorporates much which a Scottish football fan may find irrelevant, and therefore a single, clear monthly payment to get the matches they want could prove attractive.

Make no mistake: 300,000 is high. As analysts told me, this is an aspirational number, given the current cost of living crisis coupled with the constant spectre of piracy, particularly if the pricing model is prohibitive.

INFRASTRUCTURE

Launching a standalone provider in2002 would have required a carrier given the early state of the internet and lack of broadband connection. That would have been expensive and required a willing partner.

But now 94% of homes in Scotland have a broadband connection (via Ofcom, 2021) so a standard video-on-demand service in the style of Netflix or BBC iPlayer is far more possible.

Of the 2.4m homes in Scotland, 60% (1.44m) already subscribe to at least one on-demand service. A relatively new platform such as Disney+ has a 15% (300,000) market share, which gives an indication of what is possible if the product is presented properly and priced effectively.

INCREMENTAL BENEFITS

As analysts explained, there are other incremental benefits from having a captive audience subscribing specifically from Scotland, and the sponsorship opportunities that would bring.

A more refined, optimal audience would make targeting easier for brands looking to be associated with the channel at all levels of sponsorship, whether that be the value of masthead sponsor, individual spot sponsors such as those often found in American sports, or advertising run on the channel, kept to a reasonable level but providing an additional revenue stream.

Furthermore, the truly big matches such as the Old Firm games could still be packaged and provided to Sky or BBC as a separate, standalone deal. This would placate those brands who would still pay a premium for the very biggest matches and further prop up the overall revenue generation capacity of the product.

And then there’s the current media desire for first-party data. As one analyst said: “The idea that we could have first party data on all of Scottish football, and upsell them on our services, is the playbook for 2022 sports media.

“You find the audience, you collate it and then you sell it and you monetise it. You sell as much as possible, from fantasy, to data, to e-commerce, everything.”

Having access to rich data on who exactly is using the product, and how, creates a more powerful commercial operation than simply the subscribers alone. It’s a revenue stream that is difficult to estimate but one that all analysts feel is almost as integral to the model as the subscribers themselves.

Finally, the cups could remain independent and run by the SFA, providing a separate revenue stream of its own, as currently with Premier Sports.

THREATS

As analysts stressed, it is important to know what is the objective of all of this. Well, it is making sure the infrastructure of Scottish football is not only relevant and has a stable platform, but has the capacity to grow.

That’s not something that is going to happen in the current league structure. Four leagues with professional and semi-professional teams, 42 of which all compete in a market of barely five million people – a mere five per cent of our rivals in the south. Can we really support the ladder structure and continue to contribute to the top level of the game?

The debate around league restructuring is in itself an existential threat. It has been debated, discussed and shelved time and again as we continue with our 12-team, split format. But there is no doubt that familiarity breeds contempt and four matches against the same opposition every season means some matches simply blend into one another. There is nothing memorable or unmissable about that for the average fan.

But the desire to reshape the leagues and give us 16 strong top-flight teams has dragged on for almost as long as the concept of SPFL TV itself. These things are inextricably linked, and the working group that Hibs’ Ron Gordon and Aberdeen’s Dave Cormack have apparently been involved with would surely have to incorporate this into a generational rethink that puts tradition and history aside in favour of the greater good: growing the game.

As noted by one analyst with experience of negotiating league deals at the highest level in the Americas, it would require a ‘seismic’ attitude change in order to enact what is required, adding: “The league should have a duty to provide a platform for the development of young talent. Do they have a duty to preserve the history of some of these teams? Not really.”

And that also represents an undeniable threat; that English football is as interesting, if not more so, not only to Scots who have grown up watching it and may themselves travel regularly over the Border to watch it, but to young players too, who can earn more sitting in Liverpool’s under-21s than they could playing for anyone outside of Celtic and Rangers. That is a genuine problem, and one that only more revenue can resolve. Waiting for UEFA to do anything about it is a fool’s errand.

And the border isn’t quite as clear cut between Scotland and England than it is in, say, Norway or Denmark. These countries still watch other leagues, sure, but the competition is less direct than it is between Scotland and England, sharing a land mass, a language and some personalities to boot. If Scottish football wasn’t bundled into the Sky package, would they be engaged enough to pay for both separately?

And then there is the ultimate question; the aptitude of those involved. We have had Ernie Walker’s think tank, and Henry McLeish’s rank-and-file review – 10 years old now – which recommended many of the structural changes mentioned above, yet none of them have come to pass.

In 2020 McLeish accused football chiefs of ‘circling the wagons around Hampden’ and that’s the prevailing opinion from analysts: that there are simply too many self-protecting parties at play in order to instigate the transformative activity deemed necessary.

McLeish also said: “The football authorities have got to be less isolated in Scotland, less concerned about solving their own problems. They’ve got to reach out. They’ve got to have better relationships with government, better relationships with fans, better relationships with industry, better relationships with Scottish society.”

It is difficult to argue with any of that, but it is rhetoric that we have heard before, not only from McLeish, but from anyone else willing enough to provide us with insight as to where we go next. As is the case with the recent VAR vote, we are never leading, only following, happy to be given whatever we get.

SPFL TV could be a feasible future for our game. But the theory and the application seem as far away as they have ever been.